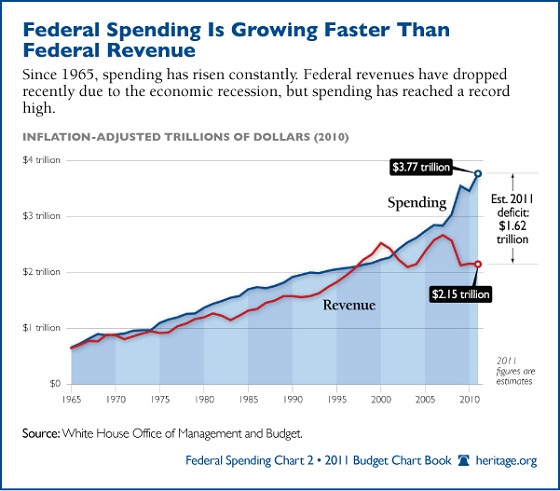

Negative Space: national debt

- Article VI

- Article Six of the U.S. Constitution transfers power from the Articles of Confederation to the Republic.

- Defaulting on our debt is an executive choice

-

If we default on any debt payments, it is because the White House has made the choice to default. There is no need to default even if the debt ceiling isn’t raised for a long time.

If we default on any debt payments, it is because the White House has made the choice to default. There is no need to default even if the debt ceiling isn’t raised for a long time.

- The Family Cow

-

If you kill the cow for steak today, you won’t have any milk tomorrow. We are digging deep into our national cash cows—taxpayers—and we’re going to soon run out.

If you kill the cow for steak today, you won’t have any milk tomorrow. We are digging deep into our national cash cows—taxpayers—and we’re going to soon run out.

- The media machine is calling me an asshole

- One side of the debt ceiling debate threatened to destroy our economy. One side just wanted to get along. One side wanted to restore fiscal sanity. Which side was extremist?

- Raising the debt limit is a major concession

- Raising the debt limit is a concession. It reduces the available revenue and makes it that much more likely that we’ll have to raise taxes.

- Robbing Peter to pay Peter… later

-

Robbing from Peter to pay Paul? Government goes one better: robbing from Peter to pay Peter. As usual, Lewis Carroll is the best writer for the layman on taxes, because Lewis Carroll is the best writer for the layman on anything. “However legal it may be to pay what never has been lent, this style of business seems to me extremely inconvenient!”

Robbing from Peter to pay Paul? Government goes one better: robbing from Peter to pay Peter. As usual, Lewis Carroll is the best writer for the layman on taxes, because Lewis Carroll is the best writer for the layman on anything. “However legal it may be to pay what never has been lent, this style of business seems to me extremely inconvenient!”

- Ryan: End oil subsidies?

- Of course we want to end oil subsidies. Maintaining oil subsidies because gas prices might rise is crazy: we pay for those subsidies, too!

- Why “we don’t have a plan” is selfishly incompetent

-

The Obama White House tells congress, “we don’t have a plan, but we don’t like your plan” when confronted with the destruction of the United States economy by 2027. Why can’t we continue to live large and then fix the problem in 2027?

The Obama White House tells congress, “we don’t have a plan, but we don’t like your plan” when confronted with the destruction of the United States economy by 2027. Why can’t we continue to live large and then fix the problem in 2027?

More Information

- Debt Limit—A Guide To American Federal Debt Made Easy.

-

“A satirical short film taking a look at the national debt and how it applies to just one family.”

- Your Wednesday Morning Dose of Doom and Gloom

-

“If rates bounce back up to just five percent—which is actually not high at all—then our interest payments get jacked up to $800,000,000,000 a year, every year, forever. And that’s just on the money we already owe. Every additional dollar we borrow gets added to the total, and the interest payments go up even higher. Every year, forever. We could balance the budget right now, and our interest payments would still be on a short slope to nearly a trillion dollars a year. Every year, forever.”